Big data is revolutionizing the FinTech industry, reshaping how companies operate, serve customers, and manage risks. With the global big data analytics market projected to reach $961.89 billion by 2032, the impact is undeniable.

Accordingly, by 2025, 80% of fintech startups will incorporate Artificial Intelligence (AI) and Machine Learning (ML) models driven by big data, accelerating their product development cycles.

From fraud detection to hyper-personalized financial services, big data is transforming traditional finance into an agile, intelligent, and customer-centric ecosystem. In this article, let’s have a look at how big data analytics transforms the FinTech industry.

The Foundation: Understanding Big Data Analytics in FinTech

Big data analytics forms the backbone of innovation in financial technology, enabling institutions to process massive datasets, uncover patterns, and make smarter, faster decisions. Through advanced analytics tools, FinTech firms can improve operational efficiency, enhance customer experiences, and gain competitive advantages in a rapidly evolving market.

What is Big Data Analytics in Financial Technology?

In FinTech, big data analytics refers to the use of advanced computational techniques and ML models to analyze enormous volumes of financial data, from transaction histories to market signals.

This data-driven intelligence empowers companies to detect fraud in real time, assess creditworthiness, and create personalized financial solutions that meet individual customer needs.

The Four Pillars: Volume, Velocity, Variety, and Veracity

The foundation of big data in FinTech rests on four key pillars:

- Volume: Massive amounts of structured and unstructured data generated daily by financial transactions.

- Velocity: The real-time speed at which data is created and needs to be processed.

- Variety: Multiple data sources, including payment histories, mobile apps, and social media interactions.

- Veracity: Ensuring the accuracy, quality, and trustworthiness of financial data.

Key Components of Big Data in FinTech

Big data in financial services spans structured data (transaction logs, balance sheets, credit scores) and unstructured data (emails, voice calls, social media activity, and alternative financial signals). Together, these datasets help institutions unlock deeper insights into consumer behavior, risk exposure, and investment trends.

Role of Cloud and Edge Computing in Big Data Processing

Modern FinTech relies heavily on cloud computing to handle vast and growing data demands. Cloud platforms enable scalability, cost-efficiency, and collaborative data sharing across global networks. At the same time, edge computing processes data closer to the source, allowing for real-time fraud detection, instant transaction verification, and faster decision-making in customer-facing applications.

Also Read: Finance KPI Dashboard Examples & Templates

Core Applications and Use Cases Transforming Financial Services

Big data analytics is not just a supporting tool in FinTech. It’s the driving force behind innovation and disruption. From fraud prevention to personalized banking, its applications are reshaping how financial services operate and deliver value.

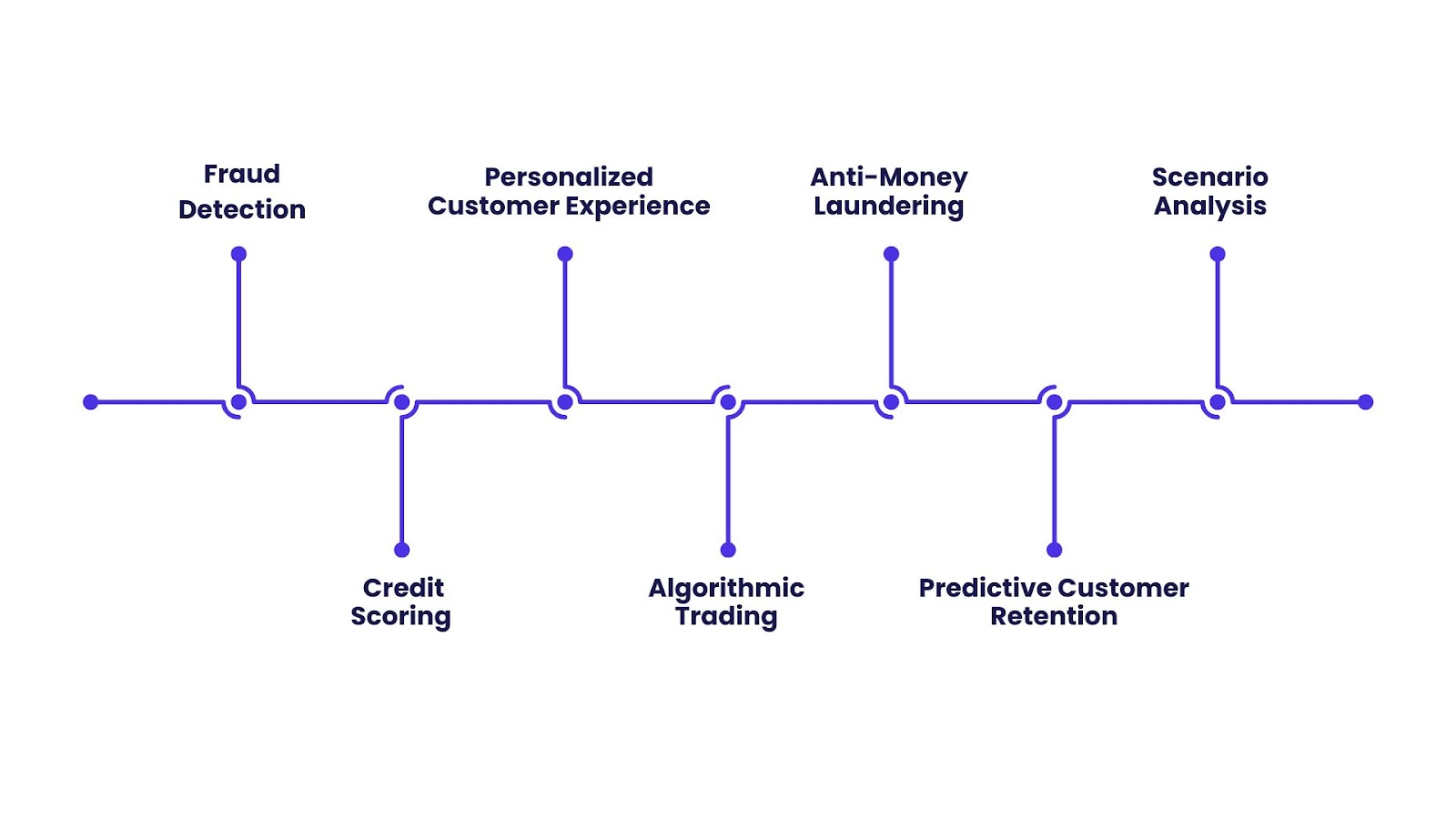

1. Fraud Detection and Prevention Systems

Fraud remains one of the most pressing challenges in financial services. Big data analytics strengthens defense mechanisms by analyzing patterns in real time.

- Real-Time Transaction Monitoring: ML algorithms flag unusual activities, such as sudden high-value transfers or transactions from unusual locations, within seconds.

- Behavioral Analytics for Anomaly Detection: Beyond basic monitoring, behavioral profiling establishes baselines for each user’s typical activity, making it easier to detect anomalies and reduce false positives.

2. Credit Scoring and Risk Assessment Revolution

Traditional credit scoring often leaves out vast consumer groups. Big data provides more inclusive and accurate risk profiles.

- Alternative Credit Scoring Models: FinTech companies use alternative data, such as utility payments, rental history, or even mobile usage, to evaluate creditworthiness.

- Real-Time Risk Evaluation: Dynamic scoring systems adjust in real time, factoring in new data streams like payment history or macroeconomic shifts.

3. Personalized Customer Experience and Product Recommendations

Big data enables financial institutions to move from generic services to hyper-personalized solutions.

- AI-Driven Customer Segmentation: Segmentation based on spending behavior, income levels, and lifestyle creates more relevant offers.

- Hyper-Personalized Financial Services: Tailored loan offers, savings recommendations, and investment products improve satisfaction and retention.

4. Algorithmic Trading and Investment Intelligence

Big data powers predictive trading models and enhances portfolio strategies for both institutions and individual investors.

- Market Prediction and Trend Analysis: AI systems process vast market signals, from news articles to global economic indicators, to forecast stock trends.

- Portfolio Optimization Through Data Analytics: Advisory platforms recommend diversified portfolios, balancing risk and return with real-time adjustments.

5. Anti-Money Laundering (AML) and Fraud Risk Scoring

Beyond simple transaction monitoring, network analysis maps relationships between accounts to identify suspicious clusters and high-risk behavior patterns.

6. Predictive Customer Retention

Financial institutions analyze behavioral signals to anticipate churn, deploying personalized retention strategies such as loyalty programs or targeted offers.

7. Scenario Analysis and Stress Testing

Banks and insurers use big data models to simulate economic downturns, portfolio shocks, or unexpected events, helping to manage risks proactively.

Advanced Analytical Techniques Powering FinTech Innovation

FinTech thrives on its ability to turn complex, high-volume data into actionable insights. This is made possible through cutting-edge analytical methods that enhance decision-making, reduce risks, and unlock new opportunities.

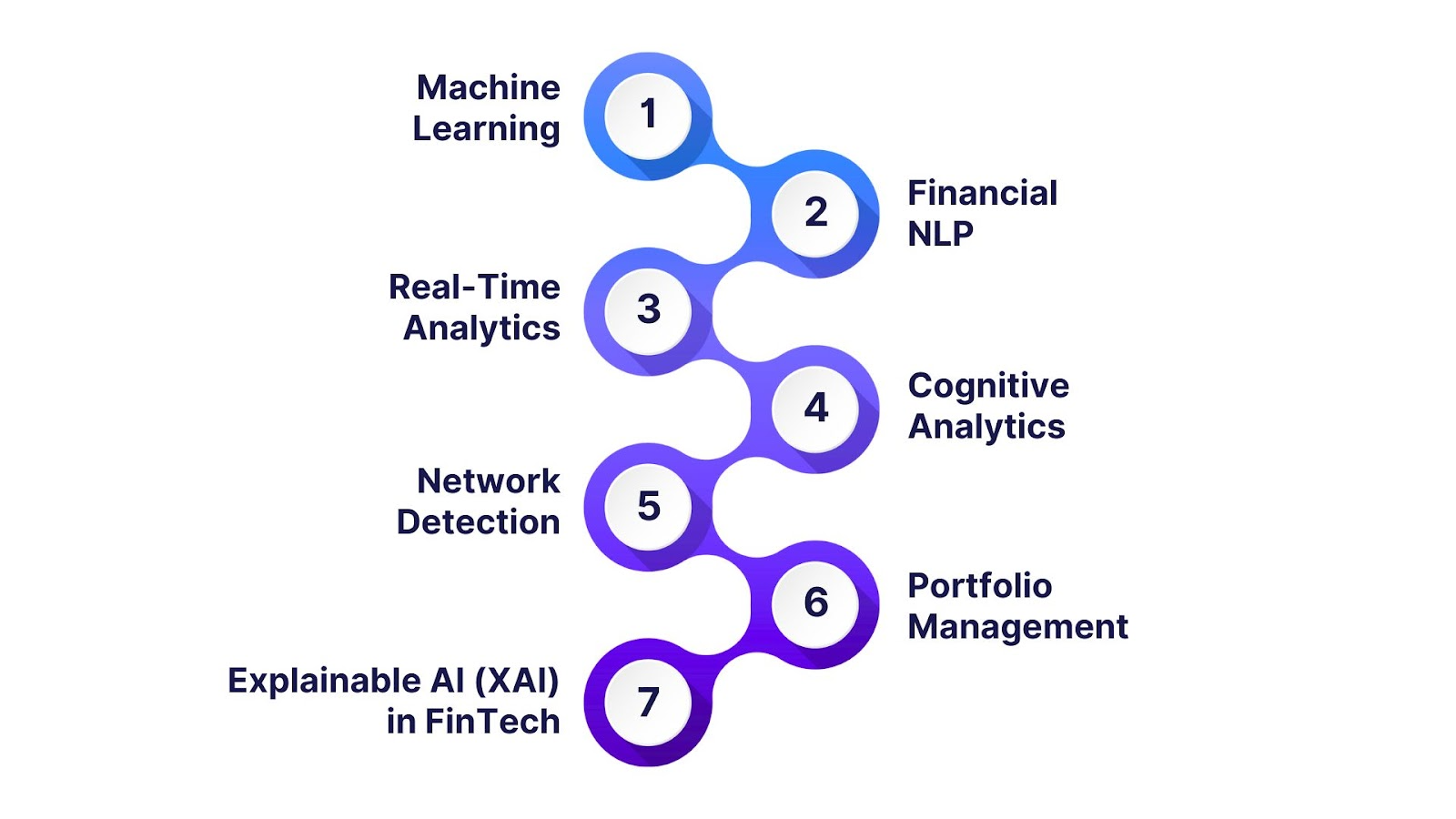

1. Machine Learning and Predictive Analytics

ML models detect patterns in financial behavior, predict loan defaults, forecast market movements, and power fraud detection systems. Predictive analytics also enables personalized recommendations, dynamic pricing, and real-time risk assessments.

2. Natural Language Processing for Financial Data

Natural Language Processing (NLP) transforms unstructured text, such as earnings reports, financial news, and social media sentiment, into quantifiable insights. Chatbots powered by NLP also improve customer service by handling queries and offering personalized support.

3. Real-Time Analytics and Edge Computing

Financial services increasingly require instantaneous insights. Real-time analytics allows for split-second decisions in fraud detection and trading, while edge computing processes data closer to its source, reducing latency and enhancing compliance with data residency rules.

4. Cognitive Analytics and AI-Driven Decision Making

Cognitive analytics combines ML, NLP, and human-like reasoning to support smarter financial decisions. It enables systems that can recommend credit limits, optimize portfolios, and automate regulatory compliance tasks.

5. Graph Analytics for Fraud and Network Detection

Fraud is rarely isolated. It often exists in networks. Graph analytics maps relationships between accounts, devices, and transactions to uncover hidden connections and detect organized fraud rings.

6. Reinforcement Learning for Trading and Portfolio Management

Reinforcement learning adapts in real time, adjusting trading strategies based on continuous feedback from the market. This enables self-optimizing trading algorithms that learn from both successes and failures to maximize returns.

7. Explainable AI (XAI) in FinTech

One of the biggest challenges in AI adoption is transparency. XAI ensures ML decisions can be understood and audited by regulators, investors, and customers, critical in maintaining trust while meeting compliance standards.

Also Read: Understanding Financial Risk Analytics: Importance and Uses

Industry-Specific Transformations Across FinTech Sectors

Big data analytics is reshaping entire FinTech sectors, driving innovation, efficiency, and trust. By tailoring insights to industry-specific needs, analytics helps companies unlock new growth opportunities while managing risk.

1. Digital Payments and Transaction Processing

Big data empowers payment providers with real-time fraud detection, faster settlements, and dynamic transaction monitoring. Analytics ensures secure, seamless payments while reducing false declines that frustrate customers.

2. InsurTech and Risk-Based Pricing Models

Insurance firms use big data to implement dynamic pricing based on individual behavior and risk profiles. Telematics data from vehicles, Internet of Things (IoT) wearables, and smart home devices enables fairer premiums and more accurate claims forecasting.

3. Digital Lending and Microfinance Platforms

Lenders use alternative data, such as mobile usage, e-commerce activity, and utility bill payments, to evaluate borrower creditworthiness. This expands financial inclusion by offering loans to previously underserved populations.

4. Wealth Management and Robo-Advisory Services

Robo-advisors rely on big data to deliver personalized investment strategies, automated portfolio rebalancing, and predictive wealth planning. This democratizes wealth management, making it accessible to a wider customer base.

5. RegTech and Compliance Automation

Compliance is a major cost center for financial institutions. Big data-driven RegTech solutions automate Know Your Customer (KYC), AML, and transaction reporting, reducing human error while meeting strict regulatory standards.

6. Blockchain Analytics for Transparency and Fraud Prevention

Big data analytics applied to blockchain enables tracking of crypto transactions, monitoring of smart contracts, and detection of suspicious patterns. This fosters greater transparency in Decentralized Finance (DeFi).

7. Predictive Insurance Claims Management

Analytics predicts the likelihood of claims, detects anomalies that signal fraud, and helps insurers optimize premium pricing. This not only lowers operational costs but also enhances customer satisfaction through faster claims resolution.

8. Peer-to-Peer Lending Risk Modeling

Big data powers advanced risk models that predict defaults in Peer-to-Peer (P2P) lending networks. By analyzing alternative data such as social media behavior and transaction histories, platforms can build trust between lenders and borrowers.

Implementation Strategies for FinTech Organizations

Successfully adopting big data analytics in FinTech requires careful planning, scalable infrastructure, and cultural alignment. Organizations that approach implementation strategically are better positioned to maximize Return On Investment (ROI) and long-term competitive advantage.

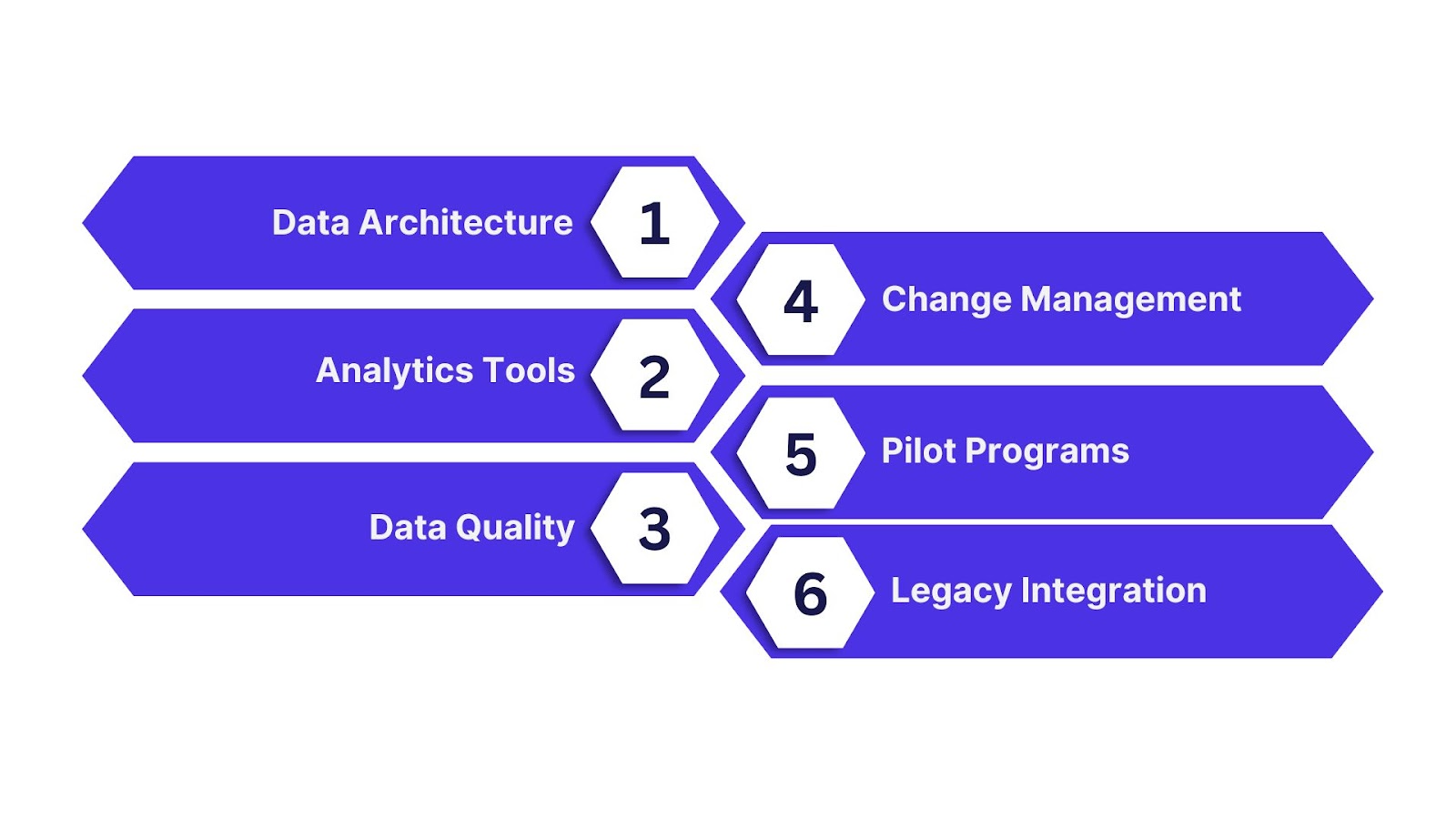

1. Building Data Infrastructure and Architecture

FinTechs need robust data pipelines, cloud storage, and scalable architecture to handle high transaction volumes. Using hybrid or multi-cloud environments ensures resilience, cost efficiency, and compliance with regional data regulations.

2. Selecting the Right Analytics Platforms and Tools

Choosing platforms that support real-time analytics, AI/ML integration, and advanced visualization is critical. Popular tools include Apache Spark, Hadoop, and cloud-native services like Amazon Web Services (AWS) Redshift, Azure Synapse, or Google BigQuery.

3. Data Integration and Quality Management

Big data is only as valuable as its accuracy, consistency, and completeness. FinTech firms must unify siloed data sources, such as transaction logs, Customer Relationship Management (CRM) systems, third-party data, while applying data cleansing, enrichment, and governance frameworks.

4. Organizational Change Management and Skill Development

Analytics transformation requires cross-functional collaboration and upskilling. Training programs in data science, AI ethics, and compliance help ensure teams can use analytics effectively. Clear communication of success stories also drives adoption.

5. Pilot Programs and Proof of Concepts

Launching with pilot projects allows FinTechs to test models in a controlled environment before scaling. These quick wins demonstrate value, secure stakeholder buy-in, and reduce risk.

6. Integration with Legacy Systems

Many financial institutions still operate on legacy core banking systems. Seamless integration ensures that new analytics tools enhance rather than disrupt existing operations, protecting customer experience during the transition.

Navigating Challenges and Regulatory Compliance

As FinTech organizations embrace big data analytics, they face regulatory, technical, and ethical hurdles that must be managed to ensure trust, compliance, and sustainable growth. Striking the right balance between innovation and oversight is essential.

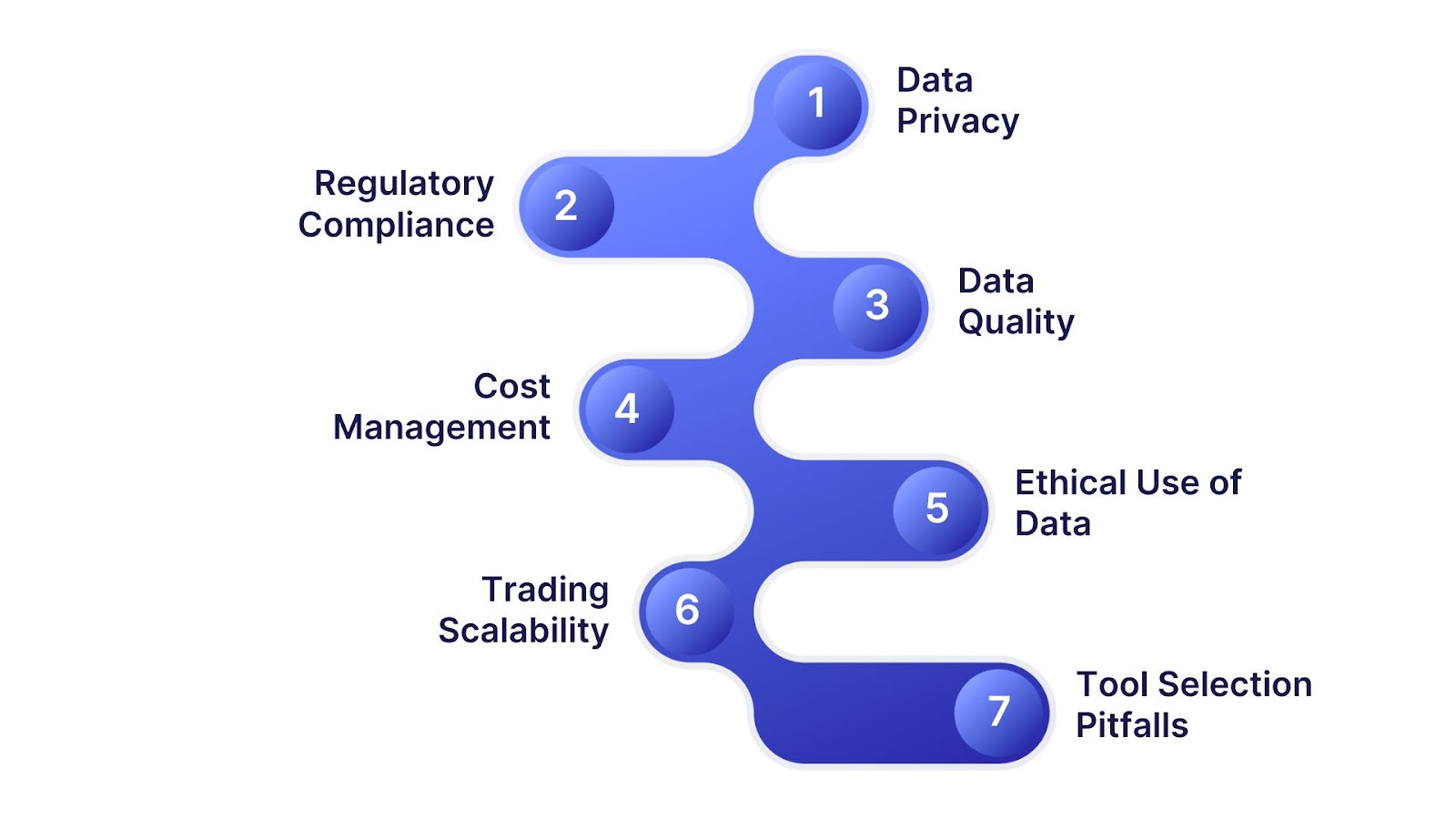

1. Data Privacy and Security Frameworks

With sensitive financial data at stake, strict data privacy and security protocols are non-negotiable.

- GDPR, CCPA, and Global Privacy Regulations: FinTech firms must comply with global privacy frameworks like GDPR (EU), CCPA (California), and upcoming data sovereignty laws in regions such as India. These regulations govern how data is collected, stored, and processed.

- Cybersecurity Best Practices for Financial Data: Encryption, multi-factor authentication, zero-trust security models, and continuous monitoring help safeguard against breaches, ransomware, and insider threats.

2. Regulatory Compliance in a Data-Driven World

As financial institutions adopt big data analytics, ensuring regulatory compliance across diverse jurisdictions becomes just as critical as leveraging data for growth.

- AML, KYC, and Regulatory Reporting: Big data enables real-time AML and KYC monitoring by identifying suspicious activity across multiple channels. Automated reporting also ensures faster compliance with regulatory agencies.

- Cross-Border Data Governance: Global FinTech operations face challenges in cross-border data transfers due to conflicting laws. Solutions include data localization, anonymization, and secure Application Programming Interfaces (APIs) that comply with regional requirements.

3. Data Quality and Infrastructure Challenges

Siloed systems, incomplete records, and high-volume streaming data can compromise insights. FinTechs must adopt data standardization, cleansing, and validation protocols, alongside infrastructure capable of handling scale.

4. Cost Management and ROI Optimization

Implementing big data analytics is capital-intensive. Firms need ROI-focused roadmaps, starting with high-impact use cases like fraud detection or risk scoring, before scaling enterprise-wide.

5. Ethical Use of Data

Predictive models must be transparent and fair, avoiding biased credit scoring, discriminatory lending, or opaque decision-making. Ethical AI frameworks ensure consumer trust.

6. Scalability Challenges with High-Frequency Trading

Processing massive, real-time datasets for algorithmic trading demands low-latency systems. FinTechs need edge computing and in-memory processing to avoid bottlenecks.

7. Vendor and Tool Selection Pitfalls

Choosing analytics vendors requires careful vetting for compliance readiness, real-time capabilities, and scalability. Misaligned tools can lead to costly reimplementation and regulatory risks.

Also Read: Financial Data Visualization: Top Charts and Techniques

Measuring Success: KPIs and ROI of Big Data in FinTech

For FinTech organizations, measuring the impact of big data analytics is critical to justify investments and ensure continuous optimization. By tracking the right metrics, firms can demonstrate both short-term gains and long-term strategic value.

Financial Performance Metrics

- Revenue Growth: Increases from cross-selling, upselling, and personalized offers.

- Profit Margins: Cost savings from fraud prevention, automation, and optimized pricing.

- Return on Investment: Direct financial return from big data initiatives versus implementation costs.

Customer Experience and Engagement Indicators

- Net Promoter Score (NPS): Improved loyalty through personalized financial services.

- Customer Retention Rate: Reduced churn thanks to predictive engagement and risk modeling.

- Average Revenue per User (ARPU): Higher value per customer due to personalized product adoption.

Operational Efficiency Benchmarks

- Process Automation Rate: Share of manual tasks replaced by big data-driven automation.

- Transaction Processing Time: Speed improvements from real-time analytics.

- Cost-to-Income Ratio: Lower operational costs relative to income due to efficiency gains.

Risk Reduction and Compliance Metrics

- Fraud Detection Accuracy: Improved anomaly detection rates with fewer false positives.

- Regulatory Compliance Score: Timely and accurate reporting for AML/KYC.

- Credit Risk Accuracy: More precise loan default predictions with alternative data models.

Building a Data-Driven FinTech Culture

For FinTech companies, technology alone isn’t enough. Success depends on fostering a culture where data-driven insights inform every decision. A strong cultural foundation ensures that big data analytics delivers sustainable value across innovation, compliance, and customer experience.

Leadership and Data Governance

- Establish executive sponsorship to prioritize analytics in strategic decisions.

- Define clear data ownership models and governance frameworks to maintain accuracy, security, and compliance.

- Build trust by implementing transparent policies for customer data usage.

Talent Acquisition and Skills Development

- Recruit data scientists, analysts, and engineers with domain-specific FinTech expertise.

- Upskill existing employees with training in AI, ML, and data ethics.

- Encourage continuous learning programs aligned with evolving technologies.

Cross-Functional Collaboration Models

- Break down silos between IT, product, compliance, and customer service teams.

- Implement data-sharing platforms that promote real-time collaboration.

- Foster a shared ownership mindset, where data-driven Key Performance Indicators (KPIs) align with business goals.

Ethics and Responsible AI Implementation

- Ensure fairness and transparency in credit scoring, fraud detection, and customer profiling.

- Adopt bias detection tools to mitigate discriminatory outcomes.

- Balance innovation with compliance, aligning with GDPR, CCPA, and financial regulations.

Cross-Functional Data Literacy Programs

- Introduce organization-wide literacy workshops to help non-technical teams understand data insights.

- Build dashboards and visualization tools that democratize analytics access.

Governance for Ethical AI and Regulatory Alignment

- Establish AI ethics boards to oversee model transparency, fairness, and accountability.

- Maintain audit trails and explainability frameworks for regulatory reporting.

Future of Big Data in FinTech

As technology advances, FinTech’s relationship with big data will continue to evolve. Emerging trends are reshaping the next decade of financial innovation:

- AI-Powered RegTech: Automating compliance and reducing regulatory reporting costs.

- Embedded Finance Analytics: Integrating lending, payments, and insurance into eCommerce platforms.

- Real-Time Personalized Banking Experiences: Offering individualized services through predictive intelligence.

- Quantum Computing for Risk Modeling: Unlocking advanced portfolio simulations and faster fraud detection.

Conclusion

The transformative powers of big data analytics lies in processing massive datasets and in enabling real-time, predictive, and actionable intelligence that drives sustainable growth.

For organizations, the key to success lies in:

- Building robust data infrastructure and governance frameworks.

- Embedding AI and automation into core financial processes.

- Overcoming challenges around privacy, compliance, and scalability.

- Cultivating a data-driven culture that empowers teams across all functions.

FinTech companies that embrace these strategies are better positioned to gain a competitive edge, strengthen customer trust, and deliver superior financial services in a rapidly evolving digital economy.

The future belongs to financial innovators who treat data as the foundation of their business intelligence strategy.

Now is the time to act. Invest in big data analytics and secure your place as a leader in the next wave of FinTech transformation.

Ready to harness the power of big data while staying fully compliant? Explore how INSIA can help your FinTech business unlock secure, scalable, and data-driven growth.